Commentary

FEM Q2 2022 Manager Letter

August 19, 2022

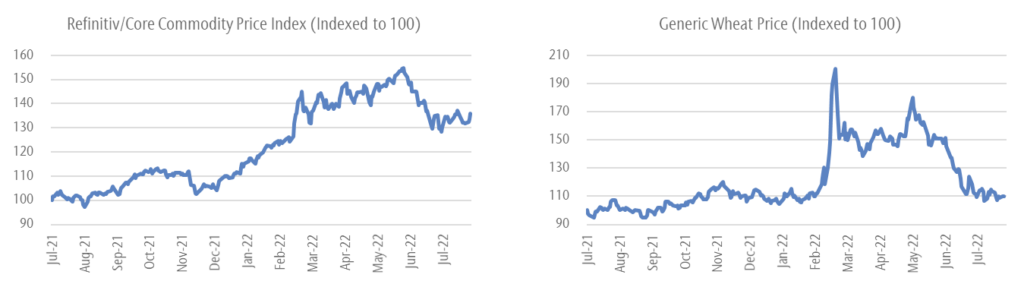

The weak absolute returns in the period reflect a very challenging investment environment for our strategy. Our focus on African and Asian companies and through-the-cycle underwriting process puts us at a cyclical disadvantage when food and oil prices experience sharp and sustained inflation. The consumer basket in our markets is over-indexed to those basic commodities, and the fiscal and balance of payment dynamics of most developing countries (where we exclusively invest) are inversely correlated to commodity prices.

While we invest in companies rather than countries, our portfolio construction process is primarily top-down driven and aims to produce a healthy mix of factors including country, sector, market capitalisation and valuation. The strategy will always be geared to domestic themes and entrepreneurial businesses which naturally results in the portfolio being under-indexed to straight commodity plays or interest rate sensitive large state-owned banks. Nevertheless, we generally do not try to make oversized single sector bets, as we have the luxury of picking exceptional businesses across a wide geography without heeding to any particular index.

As active and long-term investors, portfolio turnover comes from three sources:

- Positive thesis: a new buy or an increase in investment in an existing portfolio company, or an exit or reduce in an investment that reached a level that we deem to be full value

- Break in thesis: an exit on a break in thesis on a company due to high forecast error. These forecast errors typically come about when we underestimate competitive intensity, did not anticipate adverse regulations, or don’t agree with capital allocation decisions by management teams. Note that in these situations, the decision is typically to exit the investment, rather than reduce

- Change in environment: an exit or a reduce due to a change in the macroeconomic environment that overwhelms the positive attributes of the business we underwrote for a longer period than we think is tolerable

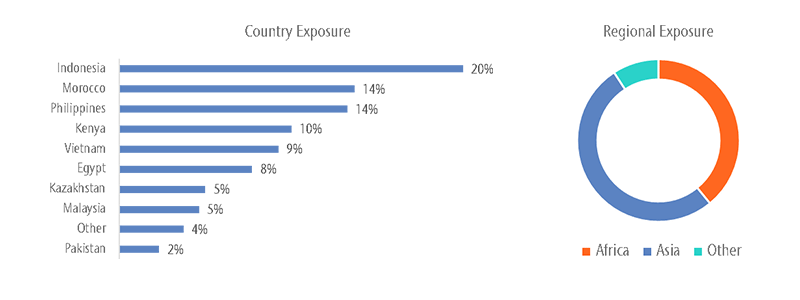

Year-to-date, the majority of our decisions can be classed under the last point. The macro environment in Egypt and Pakistan has materially worsened after the Russian invasion of Ukraine and as a result we exited two companies in the former and one company in the latter, and right sized our portfolio in both countries. We also selectively reduced exposure in Kenya in response to the same changes in the macroeconomic environment. As a result, cash has experienced the largest percentage increase in the portfolio.

More recently, we started to selectively put cash to work, focusing on companies we previously shunned on valuations and portfolio companies that have de-rated to levels that make them attractive for re-investment. All of those investments are in Asia as we still believe certain countries there will prove more resilient compared to their peers in Africa and other markets we invest in.

As global recessionary fears grow, we see a silver lining emerging in the form of softer commodity prices, which if sustained, will provide much-needed relief to developing market economies. Unless a recession proves deep, we think lower commodity prices will be a net positive to those countries. Moreover, we believe many of our portfolio companies will be resilient through a recession given the nature of the products and services they sell and/or the type of customer they target; supported by very healthy balance sheets and potential margin expansion they can experience if commodity prices continue to come off.

Figure 1: commodity prices

Figure 2: country and region exposure

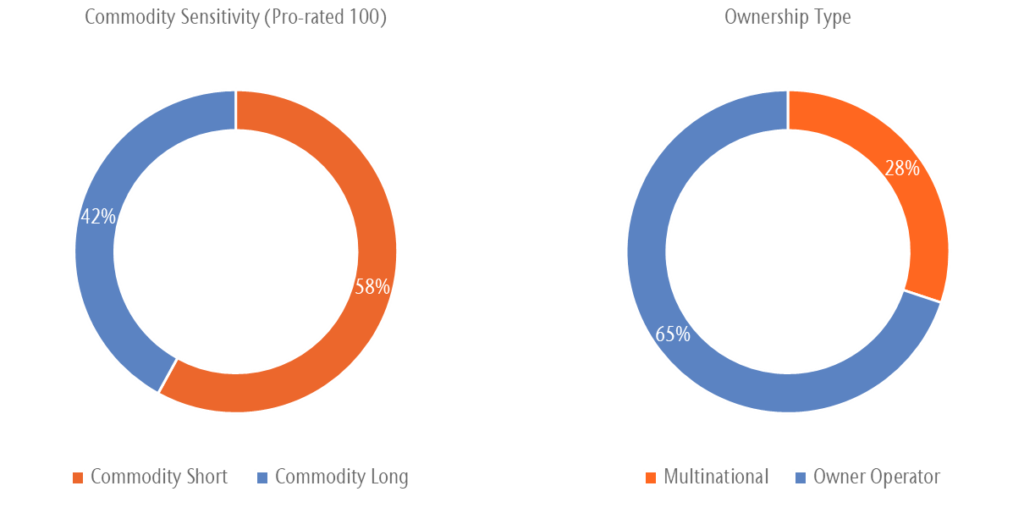

Figure 3: portfolio ownership type

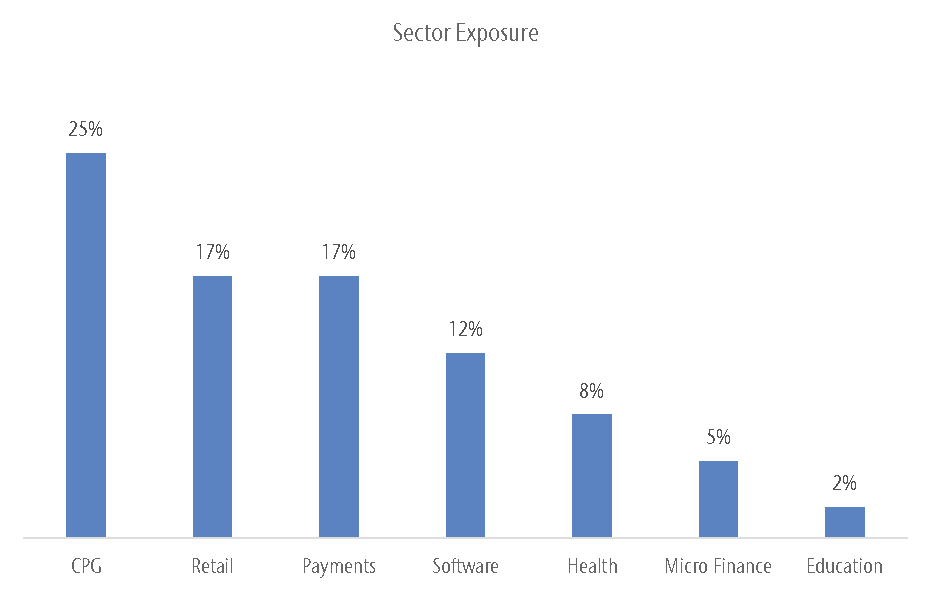

Figure 4: sector exposure

To support our investment decisions in this difficult environment, our team has visited four countries in the last two months, with a focus on portfolio companies rather than new idea generation.

Our first trip was to Morocco where we visited LabelVie, the leading grocery retailer in Morocco and a core holding in the portfolio. Our bullish view on LabelVie as the long-term winner in Morocco’s grocery market was reinforced after our trip. The company operates in a market dominated by traditional trade (+85% of the market) and a limited set of modern chained competitors. Morocco is a country with supportive demographics, solid balance of payments fundamentals, and a self-sufficient export-oriented agricultural economy which we think is always supportive for the development of the grocery retail industry.

We are most excited by Atacadão, the company’s cash & carry format, which targets traditional retail and professional buyers. The business sells bulk-packaged fast-moving consumer goods at the lowest price in the market (examples are cereals, rice, sugar, edible oils, beverages, laundry detergents, etc.). With Atacadão, LabelVie is enabling traditional trade rather than competing with it, a much less capital-intensive growth strategy. In some respects, Atacadão is disintermediating the antiquated, highly complex, and multi-layered fast-moving consumer goods (FMCG) distribution system that exist in many of the countries where we invest. These systems produces many negative externalities including inflation and wastage, which end up in higher consumer prices and lower retail margins.

After a few years of experimenting with the format, management seems to have cracked the code on Atacadão and is now looking to double store count to 26 within three years. Atacadão’s stores are approximately 30k square feet in size, carry around 4k SKUs, and are designed to maximise natural lighting to lower energy usage and keep operating costs down. The stores are strategically located near large catchment areas with supportive infrastructure to enable easy access to and from store. Each store has two sets of checkout aisles dedicated to professional buyers (cardholders, of which there are +35,000 today) or walk-in customers who are typically community shoppers.

This dual checkout system provides the company with a tremendous data asset, which they use to direct promotions or generate insights to brands (note that brands lose the data in the traditional distribution model). Uniquely, both national and global brands like Coca-Cola and Unilever deliver their products directly to Atacadão stores, reducing logistics investments and freeing existing warehouses and distribution centres for their other fast-growing retail format, Carrefour.

The Carrefour banner is another part of the LabelVie story that is delivering strong growth and gaining share in the modern grocery retail market in Morocco. The store’s focus on fresh produce, bakery, FMCG, and alcoholic beverages to generate footfall and utilise a price matching strategy with discounters to bring in shoppers from all income levels.

LabelVie’s key strength today is the ability to leverage its multi-brand platform to negotiate favourable terms with suppliers which it then transfers to shoppers (by lowering price) and shareholders (by increasing margins or subsidising store capex). We also had the privilege of spending time with the group’s new CEO, Naoual Benamar, a Procter & Gamble veteran whose appointment marks a new era for the company. Naoual spent the past three years at LabelVie before taking over from the founding CEO Zouhair Bennani, who continues to serve as Chairman.

Overall, we think the market is behind the curve on valuing the potential of Atacadão and Carrefour and see LabelVie as a multi-year secular growth story.

Figure 5: inside an Atacadão store (left) and Vergent team with LabelVie management (right)

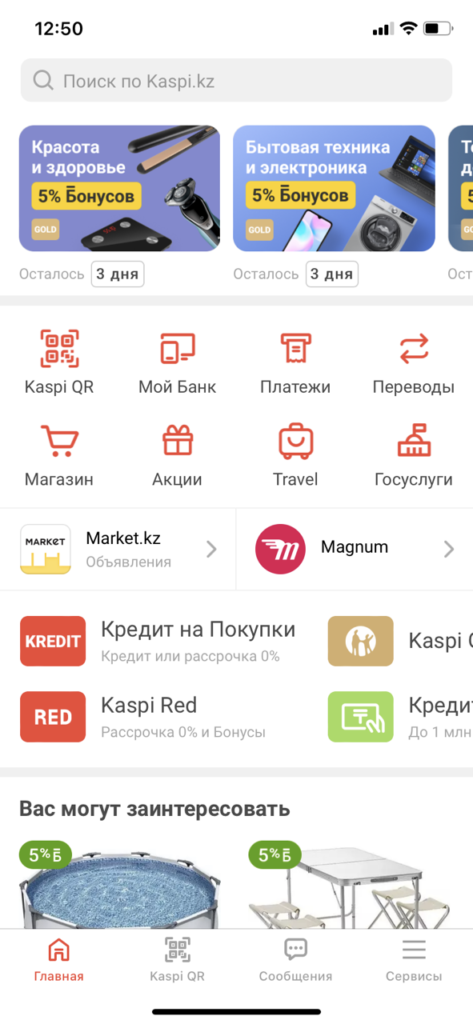

Our next trip was to Almaty, Kazakhstan where we spent nearly a week trying to learn everything we can about Kaspi.kz, a portfolio company that we discussed in detail in previous letters. We saw firsthand just how entrenched Kaspi is in the daily lives of Kazakh consumers and businesses. Whether it was a street performer, a small bakery, a Zara store in an upmarket mall or a McDonalds in a residential neighborhood, Kaspi consistently ranked as the most popular payments method for consumers. Kaspi’s operational excellence, hyperlocal strategy, obsessive focus on customer experience through Net Promoter Scores (NPS), and understanding of how incentives drive behaviour allowed them to build an unrivaled two-sided proprietary payments ecosystem so powerful that it even leapfrogged Visa and MasterCard – two of the largest and most well-funded payment networks in the world.

Kaspi is constantly looking at ways to drive value within its ecosystem. One example is in Marketplace, where Kaspi ranks as the leading online marketplace in Kazakhstan and where payments services sit neatly alongside BNPL, logistics and advertising products, all of which drive GMV growth and increase monetization.

Even in an offline environment, Kaspi leverages its merchant acquiring asset and consumer app to generate sales to merchants in-store through targeted promotions and sales activities, creating more opportunities for buyers and sellers to transact. We were fortunate to spend time with members of the senior management team who reiterated how the company is centered on its NPS score, which not only drives new product ideas but also serves as the primary KPI for management compensation. This was most evident during one of our unaccompanied visits to a Kaspi branch, where we were delighted to receive an Apple Store-like customer experience, with staff happily assisting us in navigating the very futuristic (and Kazakh/Russian language only) ATM.

We also had the privilege of spending two hours with Kaspi’s CEO Mikael Lomtadze at his office in Almaty, where we got to hear the Kaspi story from the man credited with turning the company from a failing corporate bank into the super-app of today. It is rare to get audience with Lomtadze and so we took the opportunity to ask him tough questions to which we believe we received candid and thoughtful answers. In this meeting, it became evident that Mikael’s clear vision and operational execution which focuses on customer experience, technology, and big profit pools are very much responsible for Kaspi’s success.

Kazakhstan remains in a political bind due to its proximity and links to Russia, as well as the evolving and fluid domestic political scene which we covered in the last letter. This complicates the bottom up thesis on Kaspi, but by no means breaks it. We believe the market fails to properly appreciate that Kaspi has entered a sweet spot where every product launched will have an unusually high rate of success because it is released into a scaled and highly engaged ecosystem with multiple virtuous cycles running simultaneously. We still firmly believe that the risk-reward on Kaspi sets up the strategy for significant upside down the line.

Figure 6: Kaspi QR code in retail and a photo from our visit to a Kaspi branch

Figure 7: Kaspi.Kz app interface

Later in the month, we made our way to Indonesia where we spent four days between Jakarta, Semarang, and Surabaya.

Figure 8: journey from Jakarta to Surabaya via Semarang

We met with several companies including Sido Muncul, a business we have written about extensively in the past. While we had previously visited with the company, this was the first trip to their manufacturing facilities in Semarang, in Central Java.

What stood out as soon we entered the Sido Muncul campus was the tranquil atmosphere. The facility is set among lush greenery and the scent of herbs used in production gave the place more of a yoga retreat vibe than a manufacturing facility. We were surprised to see the extent of technological advancement of the manufacturing process, given that the reins are still held by the founding family and that the primary formulation dates back to a recipe first recorded by the founding grandmother in the 1940s.

The company’s new facilities all run off a single dashboard and the German-made machinery does the rest. Production efficiency is critical to optimising yields, which leads to higher per ton values, more sales, and higher margins. While the Tolak Angin brand remains the biggest moat of the company in our view, the complications of sustainably sourcing over 900 herbs from local farmers, scaled manufacturing process, and wide distribution reach reinforce Sido’s dominance in the market. With margins that exceed Coca-Cola’s, Sido is a cash machine that still manages to grow in the low to mid-teens. Investors have long called Sido a single product company, and to a large extent it is. However, our view is this single product is extremely valuable and has a much longer growth runway than the market gives it credit for.

In addition, management’s focus on innovation and new product development can support growth beyond Tolak Angin; our channel checks in retail showed that Sido is becoming a force to be reckoned with in the supplements and vitamins category. Those new products will take time to contribute given the growth of the core Tolak Angin product but are all positive steps that reinforce brand value and set up premiumisation routes for years to come.

We also came away impressed with Sido’s sustainability initiatives: herbal waste now produces ~40% of the plant’s energy requirements and investment in solar panels is visible on plant rooftops. For a traditional herbal medicine company, Sido is progressive and modern. As a consumer company, it stands out due to its low input FX requirements, limited global raw material exposure, and strong pricing power.

Figure 9: Vergent team touring parts of the plant with Sido’s Head of Manufacturing

Figure 10: photo op with Mr. Irwan Hidayat, major shareholder and 3rd generation of the founding family of Sido Muncul

Figure 11: Sido supplement and vitamin products in retail

Our final stop was in Malaysia where we spent time with Mr DIY’s management team in Kuala Lumpur. MR.DIY is a leading multi-price point retailer with 947 stores across Malaysia. Given its name, many market participants describe it and benchmark it as a home improvement retailer. We are puzzled by that confusion as the store format, average ticket size, and pricing strategy all point to MR.DIY being more of a dollar store or fixed low-price retailer (similar to Dollar General, Family Dollar, and Dollarama). The MR.DIY store is typically about 10k square feet in size, carries 18k SKUs of fast moving non-grocery items with a focus on home, garden, hardware, and electrical. Like LabelVie, MR.DIY seems to have gotten the formula down: low prices, assortment, and locational convenience underpin their customer proposition and their attractive unit economics (payback periods of around 2 years).

The company is data-driven and uses a scientific approach to inventory management, which leads to an iterative and more efficient process over time. The company rewards its staff by distributing the excess of targeted level of margin per store. This incentive program naturally drives efficiencies and allows for more margin to be invested back into low prices. Staff are collectively incentivized to keep the stores in tip top shape. Online risk appears to be low due to the nascence of the e-commerce infrastructure at the price point that Mr.DIY clears at. The experience of Dollarama in Canada suggests that the online threat can be managed and we think Malaysia is years behind Canada in terms e-commerce penetration. Consumers may shop for electronics online, but will buy low value daily items from MR.DIY or competing store that can offer similar value. Furthermore, it is easy to see how one would leave the store buying much more than initially planned. The plethora of ‘things you didn’t know you needed until you saw them’ at very low prices is astounding.

On the ground, we observed how busy the stores are and the wide range of customers they serve, including families, young couples, and tradesmen depending on the time of the day and the location of the store. To our surprise, we saw many copycat stores that use the MR.DIY colour scheme as we drove outside Kuala Lumpur, a positive signal for the brand in our view. Like many of our portfolio companies, MR.DIY is majority founder/operator owned. Unlike all of our companies however, the founder, Mr Tan Yu Ye (YY), rarely meets investors and instead the company’s CEO Adrian Ong is given corporate and finance responsibilities while YY focuses on operations. Adrian owns 0.6% of MR.DIY (~$25 million) and is a former private equity executive who has a very good handle on the numbers and the business. This split of responsibilities is unusual but not necessarily bad for the business as each individual focuses on their areas of strength. Our investment thesis on MR.DIY was reinforced by what we observed on the ground and the strong unit economics of the business, which we will receive a boost from the reopening of Malaysia’s economy and the easing of global supply chain stresses in recent months.

Figure 12: Front of a busy MR.DIY store in Kuala Lumpur (left) and our team inspecting the aisles (right)

Figure 13: Vergent team with Mr. Adrian Ong, CEO of MR.DIY

As markets adjust to the new economic realities, we see a strong opportunity set emerging for the strategy. We believe that choppy and volatile markets offer fertile ground for fundamental stock pickers. A few of our portfolio companies also stand to benefit from this environment as their competition weakens and their bargaining position strengthens. While risks are elevated, valuations in certain areas are starting to more than bake in these risks and we are gradually and selectively rebuilding exposure in our favourite businesses.

Vergent Asset Management LLP