Blog

Sido Muncul: Underwriting a Herbal Renaissance

June 4, 2021

A Herbal Renaissance

COVID-19 has been a stark reminder of human mortality, particularly in the countries where we invest. Poor health infrastructure, strained fiscal resources, and the large informal labour market are just some of the factors magnifying its profoundly negative impact. It is easy to forget our privilege as we sit at our home offices with Amazon orders keeping the doorbell busy and fresh food only a phone tap away.

The notion of immortality has fascinated humans for millennia. Since the scientific revolution, death has become a technical challenge over a divine one[1]. Medical and societal advances have lifted global life expectancy from 46 to 72 years in the space of five decades[2]. Humans today are looking to live better for longer. In his book Homo Deus, Yuval Noah Harari talks at length on immortality, proposing enhanced-sapiens as the next evolution of our species. Once we satiate our consumption needs and wants, which have their respective ceilings, what is next? Whilst advances in genomics, artificial intelligence and prosthetics are given the most attention, what is more immediately relevant, and more accessible for the majority, are incremental life adjustments and new habit formations in day-to-day life.

“Having raised humanity above the beastly level of survival struggles, we will now aim to upgrade humans into gods, and turn Homo sapiens into Homo deus.” – Homo Deus, Yuval Noah Harari

The pandemic appears to have accelerated the pursuit for healthier and better living, evident by an uptick in demand for better-for-you products, vitamins and supplements[3]. The global supplements market is estimated to be worth over $170 billion with the herbal sub-segment contributing $7.5 billion[4],[5]. The segment has grown on the back of heightened health and wellness considerations, enhanced expression of values in purchase behaviour and greater industry commercialisation. In developed countries, having saturated the margins of society, herbal and alternative medicines are now intertwined with more conventional Western practices. The ‘herbal influence’ is certainly visible in the fast-moving-consumer-goods (FMCG) industry, yet it is geared towards the premium end of the market. We believe this speaks to the idea that ‘herbal’ has, to some extent, become a heuristic cue for premium.

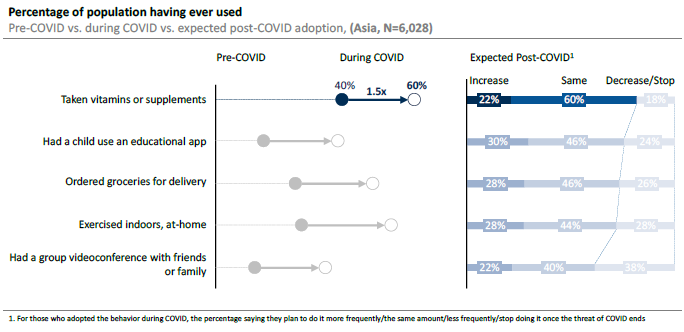

Vitamin and Supplement Consumption in Asia

We see a different picture in developing countries. In Asia specifically, we have witnessed more democratised consumption of herbal products and supplements as entrepreneurs, brand owners and even spiritual leaders have taken to formalising traditional remedies[6].

India is home to one of the best examples of this, with the modernisation and commercialisation of Ayurveda, an alternative medicine system, in everyday FMCG products[7]. Against the backdrop of rising Hindu nationalism and a democratisation of route-to-market accessibility, both local (Dabur, Himalaya, Emami, Marico and Patanjali) and multinational corporations (Nestle, Colgate, Unilever) have capitalised upon this structural trend. India has seen a culmination of factors, which together have propelled the segment to over $5 billion, with 76% of Indian households using Ayurvedic products for personal and health care needs[8]. COVID-19 has accelerated the growth of the Ayurvedic segment, not only for edible categories but also home and personal care items. India’s Health and Welfare Ministry even issued guidelines for recovering COVID-19 patients that included the consumption of Ayurvedic products.

Ayurvedic FMCG Products

Colgate is one of the many multinational brands that have capitalized

on the growth in Indian alternative medicine market

In Indonesia, a market where we are invested, we have witnessed a similar trend. Increasingly consumers are allocating their marginal dollars to modern and branded versions of traditional remedies as well as products that more closely align with their religious and cultural identities.

Much like Ayurveda in India, Jamu is an ancient and indigenous form of care. It predicates that if ailments come from nature, their cure should too. Jamu comprises of a blend of tonics, ointments, oils and pills made from ginger, turmeric, tamarind, honey and other local spices found on the 17,000 island archipelago. Indonesians believe that these concoctions strengthen the immune system and serve as both a preventative and remedial solution to common illnesses. Historically, it was sold in traditional outlets, mainly by elder women (Jamu Gendong), sometimes in unhygienic conditions. According to the Ministry of Health, the Jamu industry is worth $2.7 billion and is consumed regularly by 49% of the 260 million population[9]. In contrast to Ayurveda however, Jamu has yet to benefit from the same global exposure, without a dedicated evangelist (see Baba Ramdev of Patanjali[10]) or full integration into mass market FMCG.

Jamu Gendong and Modern Jamu-inspired Products

Conventional wisdom stipulates that Jamu is primarily consumed by elder generations, with younger, cosmopolitan consumers generally aspiring to international lifestyle products and wellness solutions[11]. What we have seen recently however, is a renewed interest in these traditional and herbal products as part of a longer-term trend. Jamu Cafes and Bars have emerged in Jakarta and there are dozens of companies that incorporate Jamu into both their edible and inedible products. The pandemic has also supported Jamu’s revived popularity amongst Indonesians[12]. President Joko ‘Jokowi’ Widodo publicised his morning Jamu routine and Dr. Chairul Anwar Nidom, Airlangga University, suggested drinking Jamu could boost immune systems. It seems as though global trends coupled with strong inherited tradition is leading to the growth of this budding industry.

Capitalising on the opportunity

One beneficiary of this herbal renaissance is our portfolio company, Sido Muncul (SIDO), a leading producer of herbal supplements in Indonesia. SIDO has built a business in modernizing a family recipe dating back to 1941; building a brand that now captures over 70% of its market. The company’s flagship product Tolak Angin is mainly used to treat ‘Masuk Angin’, a local ailment, but it is also taken to boost immunity[13]. Masuk Angin is not a medical term, but instead a colloquial term for the collective feeling of fever, chills, muscle ache and discomfort associated with the onset of what Westerners would call a cold. Its general applicability implies Tolak Angin is not limited to solving a single symptom, therefore use cases are plentiful.

The company is run by a professional team of third generation family members (who own 60%), complemented by seasoned executives in sales, distribution and finance. Regional Private Equity (PE) firm Affinity Partners took a stake in January 2018, and now hold 21% in the listed business. Affinity have supported management, whose natural strengths are in sourcing and production, by adding expertise in finance and logistics.

Sido Muncul Flagship Product – Tolak Angin

What is most striking (and attractive) about SIDO is the phenomenal margins it generates on Tolak Angin (+75% gross profit margins) which leads to a company level profitability profile that is far superior to even that of Coca Cola. Just like Coke, Tolak Angin has ultimate pricing power in its category and that is reflected in an approximate 20% premium on a per unit basis compared to its competitors. Unlike Coke, Tolak Angin does not have a strong second competitor and enjoys the benefits of being in a category that multinationals have found difficult to crack.

Operating Margin Comparison

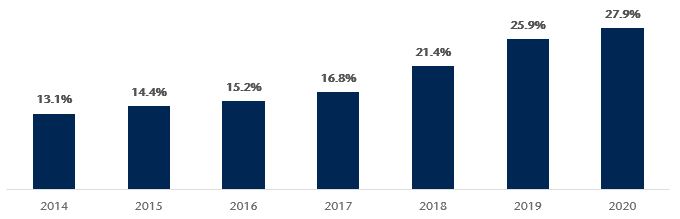

Return on invested capital more than doubled in the last six years as a result of SIDO scaling up manufacturing, optimising distribution, and making good capital allocation decisions. This has led to substantial free cash flow generation which management has been progressively paying out in dividends.

Return on Invested Capital (%)

Despite the impressive revenue and profit margin performance to date, we see more growth for SIDO ahead. The company is now building on demand in the East of the country where per capita consumption is one quarter of that in Greater Jakarta. In addition, management have outlined an export strategy focused on the Philippines, Nigeria, Malaysia and Saudi Arabia where its products have an existing following. Building on the strength of the brand, the company is launching new higher value-added products through new formulations, formats and flavours. On the margins side, we see scope for further efficiency gains as factory utilisation improves, raw material pricing is standardised and the as innovation pipeline of high value products comes to market.

Vergent Asset Management LLP

[1] https://www.theguardian.com/books/2020/apr/20/yuval-noah-harari-will-coronavirus-change-our-attitudes-to-death-quite-the-opposite

[2] https://ourworldindata.org/

[3] https://www.ft.com/content/fbcfe8df-4ab9-47c3-974e-320e0d320d19

[4] https://www.globenewswire.com/news-release/2021/01/19/2160500/0/en/Industry-Statistics-Global-Dietary-Supplements-Market-Size-Will-Grow-to-USD-306-8-Billion-by-2026-Says-Facts-Factors.html

[5] https://www.prnewswire.com/in/news-releases/herbal-supplement-market-size-usd-8983-6-million-by-2026

[6] https://www.bloomberg.com/news/features/2018-03-15/this-multibillion-dollar-corporation-is-controlled-by-a-penniless-yoga-superstar

[7] https://www.ayurveda.com/resources/articles/ayurveda-a-brief-introduction-and-guide

[8] Note that the industry is highly informal implying a market size much greater than official statistics state.

[9] Given the industry is overwhelmingly traditional, the $2.7bn figure likely falls short of its true size.

[10] https://www.bloomberg.com/news/features/2018-03-15/this-multibillion-dollar-corporation-is-controlled-by-a-penniless-yoga-superstar

[11] https://www.channelnewsasia.com/news/asia/indonesia-jamu-herbal-cafe-hip-13017214

[12] https://www.thejakartapost.com/news/2020/04/29/market-reports-paint-a-bright-post-pandemic-future-for-indonesian-jamu.html

[13] https://www.vice.com/en/article/z4na7a/we-asked-an-expert-to-explain-medically-what-happens-when-you-catch-masuk-angin

DISCLAIMER