‘Utility: the state of being useful, profitable or beneficial’

Ask any respectable scientist or engineer how they achieved distinction, and they will likely tell you that they stood on the shoulders of giants. Such is the nature of their fields – you build upon the work of your predecessors. However, it would be a mistake to think that this is the only approach to development. Sometimes the best solutions come from scrapping the previous script, redefining the problem and standing on your own two feet.

Take the modern banking system as an example. While it has been tweaked and nudged into the digital age, the system is still – at its core – an iteration of a centuries old industry. If you look closely enough, not a lot has changed from the principles set out in the 15th century (and still employed to this day) by the Banca Monte dei Paschi di Siena. It is a rather extraordinary idea when you think about it, and one that stokes an interesting discussion internally when we ask ourselves what if we had the luxury of redesigning the system from scratch? Would we arrive at the same modern day setup? Would we see a need for a network of bank branches, for instance? Would utility bills and signatures be our preferred means of identity authorization?

In our view, it is a resounding no. But such is the consequence of an iterative process and a series of shortsighted ‘quick fixes’ that seldom appear shortsighted at the time (e.g. replacing cheques with debit cards); they assume a very different perspective when we take a step back. If we deconstruct ‘banking’ into the core utility on which it was designed – the store of wealth and the transfer of money – then it becomes apparent that the major providers of utility in most markets are no longer the banks. The value proposition is shifting from ‘where is the safest place to store my money’ to also include ‘what is the most seamless and cost effective way to transfer and manage my money’. The once dominant financial institutions are seeing their power eroded by technologically enabled disrupters, leveraging off mobile solutions, data and APIs.

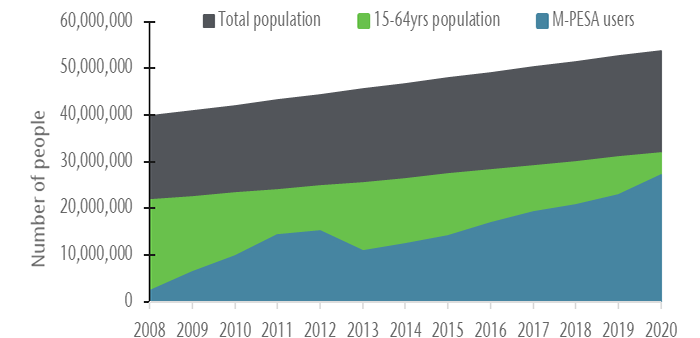

Somewhat surprisingly, one of the best examples of this trend can be found in Kenya. It is rare that the markets in which we invest harbor a best in class operator – particularly in disruptive sectors, and in a global context – but mobile network operator, Safaricom, is one exception. Through their mobile money network, M-PESA, they have almost single handedly brought more than 30 million Kenyans into the digital payments age, in what has been one of the world’s greatest advances in financial inclusion1.

M-PESA, as the name suggests (M = ‘mobile’; PESA = ‘money’ in Swahili) was one of the earliest mobile money products in an industry that has since ballooned to include more than 1 billion people globally, of which more than 50% are located in Sub-Saharan Africa2. The idea is simple – a digital wallet that is linked to a mobile phone. There are no banks involved. No account numbers. No etching your name onto the back of a card. An individual’s e-wallet links directly to their SIM, meaning a phone number is all that is needed to send and receive money.

If you lived in Kenya in 2005 there was a 70% chance you didn’t have a bank account3. Today, as an adult in Kenya, there is almost 100% chance that you have an M-PESA account and have transferred money digitally to somebody else in Kenya. In 2019, the total value of transactions that ran through M-PESA was almost 15% higher than Kenya’s entire $96 billion GDP. That is a whopping 8 billion unique transactions, or more than 150 transactions per person. For context, in the same year Germany recorded less than 60 cashless transactions per person4. Money enters and exists the M-PESA ecosystem through a network of ‘agents’, which mainly comprises authorized dealers, but also includes retailers such as petrol stations, supermarkets and registered SMEs. There are over 200,000 of these agents – that is more than every bank branch, ATM, currency exchange and microfinance institution in Kenya combined5.

Source: World Bank; Vergent Asset Management LLP

Note that Safaricom changed the definition of M-PESA users in 2013 from ‘Total Number of Users’ to ‘Users that have used M-PESA at least once in the last 30 days’. Under the former definition, there are over 30m M-PESA users today.

The early signs of M-PESA’s infiltration – and to some extent, redefinition – of the banking system are clear. Consider M-Shwari, an application built on M-PESA through which consumers can apply for up to KES 50,000 (roughly USD $450) in short-term loans. When M-Shwari launched in November 2012, approximately 700,000 Kenyans had an outstanding personal loan. Just three months later, M-Shwari had signed up a staggering 2.9 million customers, which rose to 5 million by the end of the year and almost 10 million a year later6. For the bank that underwrites the loans – NCBA Bank – just under 50% of all loans disbursed in 2019 were through M-Shwari 7.

KCB Bank has enjoyed similar success. Just one year after launching KCB M-PESA, an almost identical short-term loan product, their customer base had more than doubled to 9 million people. That is one of the largest banks in East Africa, having taken 115 years to amass its first 4 million customers, taking just 12 months to add 5 million more8. It is quite remarkable to witness even the most established, multi-centurial banks such as KCB sliding down the value chain of their own industry.

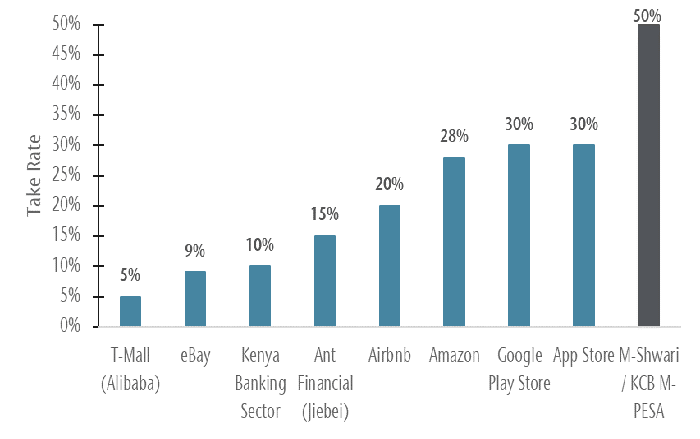

As fundamental investors, we assess the strength of our companies through an array of qualitative and quantitative methods. Sometimes, however, it can be just as useful analysis to employ a far simpler framework. History has consistently proven (across both capitalist and socialist systems) the old adage that money is power. Less discussed, albeit a slight subtlety, is the opposite. Power is money – the idea that those with influence and control can lever their advantage in order to benefit financially. For some companies, we can gauge this power quantitatively by analyzing the take rate – the percentage commission charged per transaction. There are a number of factors that go into the take rate, but generally those with a stronger grip on their respective industries are able to demand a higher rate.

In this context, it is worth remembering that fundamentally, M-PESA is nothing more than a digital distributor. Consumers pay a small fee in return for the ability to distribute money to any other M-PESA user in Kenya. For financial products such as M-Shwari and KCB M-PESA, the underwriting banks pay for the privilege of distributing their products through M-PESA. The chart below compares the take rate that M-PESA earns on these financial products with some of the largest physical and digital distributors in the world. It is a surprising data point, but one which undeniably evidences the power that M-PESA holds over the Kenyan banking sector.

Source: Vergent Asset Management LLP

T-Mall includes fees for paying through AliPay. e-Bay is the blended rate for the US and international businesses. Kenya Banking Sector is calculated as the average yield for the last three years, adjusted for provisions for bad loans. Jiebei is an unsecured, consumer loan product. The rate given is on an annualized basis. Amazon is inclusive of 3P commissions, logistics fees and advertising fees.

What M-PESA has done for the financial development of Kenya has been nothing short of extraordinary. And what is most exciting is that we see this as just the start, the prelude to what is shaping up to be the most profound chapter of M-PESA’s story so far. As Ol’ Blue Eyes, Frank Sinatra, would say – “the best is yet to come”. M-PESA 2.0 will grow into its role as the core financial ecosystem in Kenya, and the global poster child for how technology and connectivity can expose the frailties of the modern banking system. We expect it will become much more than a convenient way to transfer money. Consumers will be able to pay for almost any good or service, settle bills and seamlessly send money from abroad; the government will collect taxes and pay public sector employees; banks will use it as their preferred channel to distribute credit, insurance and other financial products. Put another way, we believe M-PESA is on track to become the core provider of financial utility in Kenya.

We hasten to add that the next leg of M-PESA’s journey will not be all blue skies and rainbows. There will of course be storms ahead, as regulators and policy makers play catch up, and as the retail banking sector fights to stay relevant. Nevertheless, we are confident that M-PESA has what it takes to navigate these challenges successfully. Safaricom is, and has always been, our biggest bet. A company that from a small corner of Africa is spearheading one of the most powerful digital revolutions on the planet.

Vergent Asset Management April 8, 2021

1. Source: Safaricom, company accounts 2. Understanding why mobile money has been so disproportionately successful in Africa could be the subject of another paper entirely, and we will refrain from doing it an injustice by skimming over the details here. For the curious reader, we highlight what we think have been the three key ingredients: i) markets that have low banking penetration; ii) economies that are heavily reliant on cash; iii) populations that exhibit high rural density. 3. Source: GSMA Report, 2015 4. Source: Deutsche Bundesbank data 5. Source: CBK data 6. Source: FSD Kenya 7. Source: NCBA company accounts; Safaricom company accounts 8. Source: KCB company accounts

DISCLAIMER

These materials (“Presentation”) are presented by Vergent Asset Management LLP <(“Vergent”)>. This Presentation is furnished on a confidential basis for informational and illustration purposes only. This Presentation is intended for the use of the recipient only and may not be reproduced or distributed to any other person, in whole or in part, without the prior written consent of Vergent.

Vergent Asset Management LLP is registered in England and Wales with its registered office address at 8th Floor, 1 Knightsbridge Green, London SW1X 7QA, United Kingdom (Companies House number OC418829) and is authorized and regulated by the Financial Conduct Authority (FRN: 791909).

This financial promotion is issued by Vergent Asset Management which is authorized and regulated by the Financial Conduct Authority (‘FCA’). Past performance is not indicative of future results. The value of your investment may go down as well as up and you may not receive upon redemption the full amount of your original investment.

THE PERFORMANCE PRESENTED HEREIN IS NOT INDICATIVE OF FUTURE RESULTS. The performance results contained herein are for informational purposes only, and are not meant to imply that Vergent’s trading programs will produce results similar to the performance results contained herein. There can be no assurance that Vergent or any account or product advised thereby will or is likely to achieve any results shown. There can be no assurance that such trading programs will make any profit at all or will be able to avoid incurring substantial losses. No representation is made that Vergent’s investment processes or investment objectives will or are likely to be successful or achieved.

Certain information contained in this Presentation is based on information obtained from third-party sources that Vergent considers to be reliable. However, Vergent makes no representation as to, and accepts no responsibility for, the accuracy, fairness or completeness of the information contained herein. The information is as of the date indicated and reflects present intention only. This information is subject to change at any time, and Vergent is under no obligation to provide you with any updates or amendments to this Presentation. The information contained in this Presentation is not complete and does not contain certain material information about the trading programs described herein, including important risk disclosures. Accordingly, this Presentation must be read in conjunction with, and is qualified in its entirety by, such other disclosure documentation as may be provided by Vergent from time to time in connection with a prospective investment. An investment in the strategy described herein may not be suitable for all clients, and before allocating any assets to the strategy or strategies, you should thoroughly review the terms and disclosures the strategy and consult with your professional advisor(s) to determine whether an investment in the strategy is suitable for you in light of your investment objectives and financial situation.

This Presentation may contain opinions pertaining to securities, financial products, transactions and investment strategies, and such opinions may differ from one to another. Any opinions, assumptions, assessments, statements, market commentary or the like (collectively, “Statements”) regarding past, current and/or future market conditions, themes, trends or events or which are forward-looking, including regarding portfolio characteristics and limits, constitute only subjective views, beliefs, outlooks, estimations or intentions of Vergent, should not be relied on, are subject to change due to a variety of factors, including fluctuating market conditions and economic factors, and involve inherent risks and uncertainties, both general and specific, many of which cannot be predicted or quantified and are beyond Vergent’s control. Future evidence and actual results could differ materially from those set forth in, contemplated by, or underlying these Statements, which are subject to change without notice. In light of these risks and uncertainties, there can be no assurance and no representation is given that these Statements are now, or will prove to be, accurate or complete in any way. Vergent undertakes no responsibility or obligation to revise or update such Statements. Statements expressed herein may not necessarily be shared by all personnel of Vergent. You acknowledge that you are capable of independently analyzing such Statements and the other information presented herein using your own expertise, due diligence and decision making, and you are solely responsible for any investment decisions made through your use of such Statements or other information and for any and all trading results achieved thereby, whether for your own account or on behalf of your clients.

This Presentation is not an offer to buy or sell, nor a solicitation of an offer to buy or sell any security or other financial instrument, or to invest assets in any account, advised by Vergent. An investment in any account advised by Vergent may be made only by qualified clients after receipt of formal investment management documentation and disclosures from Vergent, and only in those jurisdictions where permitted by law. Vergent’s investment strategies have management fees and operating expenses that would reduce returns to a client. Operating expenses include items such as custodial fees for segregated accounts and for pooled vehicles would also include charges for valuation, audit, tax and legal expenses. Such additional operating expenses would reduce the actual returns experienced by investors in segregated accounts and pooled vehicles. Any client must be able to bear the risks involved in any potential investment and must meet the suitability requirements relating to its participation in the Trading Programs.

Financial indices are shown for illustrative purposes only, may not be available for direct investment, are unmanaged, assume reinvestment of income, do not reflect the impact of any management or incentive fees and have limitations when used for comparison or other purposes because they may have different volatility or other material characteristics (such as number and types of instruments) than the investment strategies described herein. Vergent’s investment strategies are not restricted to the instruments comprising any one index.

Vergent is not and does not purport to be an advisor as to legal, taxation, accounting, financial or regulatory matters in any jurisdiction. The recipient should independently evaluate and judge the matters referred to in this Presentation. Net performance figures are stated after estimated management fees and transaction costs but before operating expenses. Operating expenses include items such as custodial fees for segregated accounts and for pooled vehicles would also include charges for valuation, audit, tax and legal expenses.

Third-party data providers

This report may contain information obtained from third parties including: Merrill Lynch, Pierce, Fenner & Smith Incorporated (BofAML), S&P Global Ratings, and MSCI.

Source: Merrill Lynch, Pierce, Fenner & Smith Incorporated (BofAML), used with permission. BofAML permits use of the BofAML indices related data on an “As Is” basis, makes no warranties regarding same, does not guarantee the suitability, quality, accuracy, timeliness, and/or completeness of the BofAML indices or any data included in, related to, or derived therefrom, assumes no liability in connection with the use of the foregoing, and does not sponsor, endorse, or recommend Vergent, or any of its products.

This may contain information obtained from third parties, including ratings from credit ratings agencies such as S&P Global Ratings. Reproduction and distribution of third party content in any form is prohibited except with the prior written permission of the related third party. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and are not responsible for any errors or omissions (negligent orotherwise), regardless of the cause, or for the results obtained from the use of such content. THIRD PARTY CONTENT PROVIDERS GIVE NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. THIRD PARTY CONTENT PROVIDERS SHALL NOT BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, EXEMPLARY, COMPENSATORY, PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES, COSTS, EXPENSES, LEGAL FEES, OR LOSSES (INCLUDING LOST INCOME OR PROFITS AND OPPORTUNITY COSTS OR LOSSES CAUSED BY NEGLIGENCE) IN CONNECTION WITH ANY USE OF THEIR CONTENT, INCLUDING RATINGS. Credit ratings are statements of opinions and are not statements of fact or recommendations to purchase, hold or sell securities. They do not address the suitability of securities or the suitability of securities for investment purposes, and should not be relied on as investment advice.

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. MSCI makes no express or implied warranties or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. This report is not approved, reviewed or produced by MSCI.

Poor access to credit continues to be a major growth inhibitor for many developing markets. We explore how platform businesses are attempting to bridge the funding gap through the digitalisation of financial services. We present kaspi.kz an illustration of a platform centred on consumer credit, that is driving both societal change and attractive returns for shareholders.

In this paper, we examine the rising trend of Saudi nationals leading Saudi-listed companies. Our work shows that developing an understanding of the people and culture of Saudi companies provides valuable insights on the quality of those companies.