Blog

Credit where credit’s due

January 19, 2023

The story of Little Red Riding Hood is perhaps the most implausible of all the pre-17th century European folk tales. Just how – a rational mind may presume – does a little girl mistake a ravenous wolf for her own grandmother? Like many such fables, the beauty in the Grimm brothers’ work lies in the extraction of rich metaphorical meaning from absurdity. Timeless lessons that have a habit, for those paying attention, of occasionally popping up in unexpected areas of our lives like a sagacious Whac-a-Mole. While Little Red Riding Hood is hardly a fulsome guide to investing, her ill-fated demise due to a case of mis-identity may still offer a lesson for investors.

As fundamental equity investors, it is critical that our decisions stem from objective reasoning. Spending each day striving to achieve the clarity of thought that comes with truly unbiased, matter-of-fact thinking, honed by experience and devoid of prejudice, is key not only to our long-term success but also in upholding the fiduciary duty to our clients.

It is why our philosophy centres on two simple ideas: invest with conviction and act with humility. The guiding principles behind each of our decisions that help us uncover wolves concealed amongst even our highest conviction ideas, and prevents deception from the seemingly familiar becoming – ironically – all too familiar.

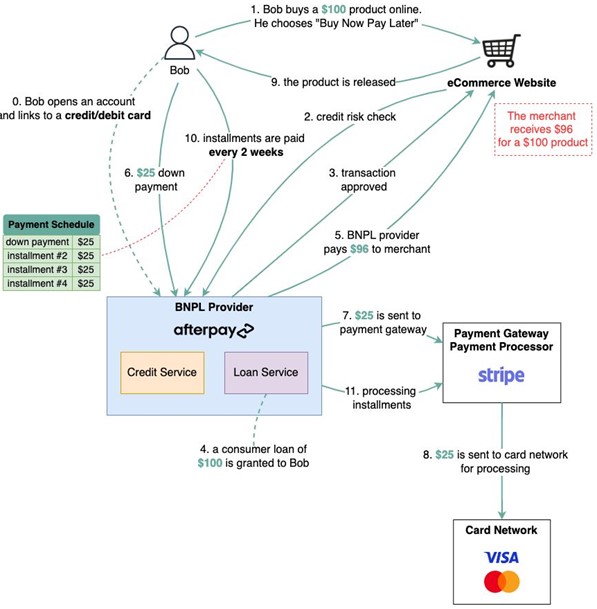

Buy-now-pay-later (BNPL) is one concept that we believe can be particularly deceptive. To the unassuming consumer, BNPL is wonderfully ingenious. Credit risk for your transaction is shouldered by the merchant from whom you purchase. It looks, smells and tastes like free money. Only alas! On closer inspection we find that BNPL is in fact just a craftily marketed, dolled up version of the same age-old credit process. Soft pastel colours and smiling millennials may have replaced images of burly debt collectors demanding pounds of flesh, but the core underlying credit agreement between consumer and lender remains unchanged. Missed payments will still result in the same letters in the post, demanding the same penalizing late fees. And opening them will still provoke the same sense of incredulity as you jump up and shout, “Oh my! I didn’t realise what big teeth you have!”

Figure 1: A typical BNPL transaction

Contextualising BNPL as a branch of consumer credit is a prerequisite to appreciating its value. The ongoing arms race between technology giants Grab, GoTo and Sea Ltd over Southeast Asia’s 120 million Indonesian labour force participants who do not own a credit card is the archetype of the modern fintech battle that we see across many of our markets. There are millions of people in Egypt, Vietnam, Philippines, Nigeria, Kenya and Bangladesh without access to consumer credit, but poor pre-existing infrastructure makes it difficult for highly focused credit products such as BNPL to gain traction.[1] Here, the spoils of war will not be won on credit alone. Funding gaps of such depth and complexity must instead be addressed by a broad arsenal of fintech services including digital banking, cashless payments, credit reporting and cross-border transactions.

Alibaba’s Alipay is arguably the best example to-date, and its success in China has created a blueprint for many platform businesses within our markets. A collection of fledgling financial Megazords working to refine the configuration of their autonomous product constructs. For many it remains a work-in-progress. However, there are exceptional cases that indicate some may have found a winning formula.

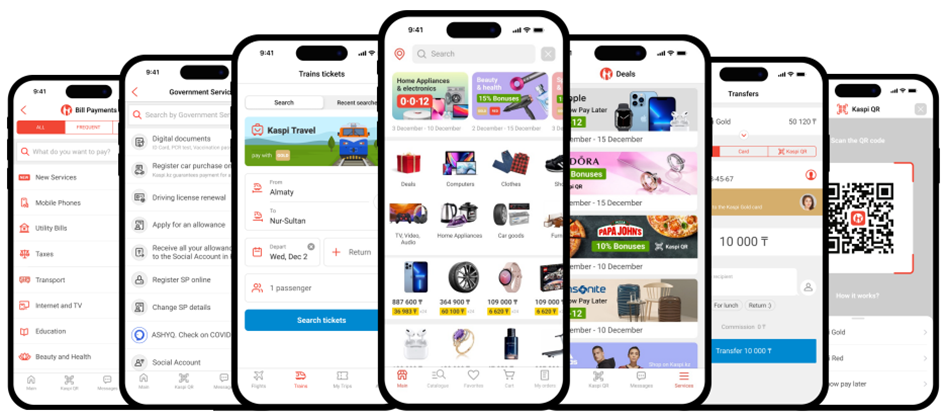

Nestled away in a market of just 19 million people, Kaspi.kz has built a formidable application that boasts a user base comprising over 95% of the adult population of Kazakhstan. What originated as a humble Tier 2 bank has emerged over the last decade as the largest payment network, e-commerce platform and consumer finance business in the country.[2] Today, Kaspi.kz processes more transactions in Kazakhstan – where over two thirds of all transactions are cashless – than Visa and MasterCard combined.[3] Online purchases through the 260,000 active merchants on the platform account for over 70% of the entire e-commerce market.[4] And in 2021 they distributed over twice the amount of consumer loans compared to the largest and most systemically important bank in the country. In short, Kaspi.kz is not just a part of the fintech revolution in Kazakhstan. It is the revolution.

Figure 2: Kaspi.kz has multiple payments, e-commerce and credit products within a single application

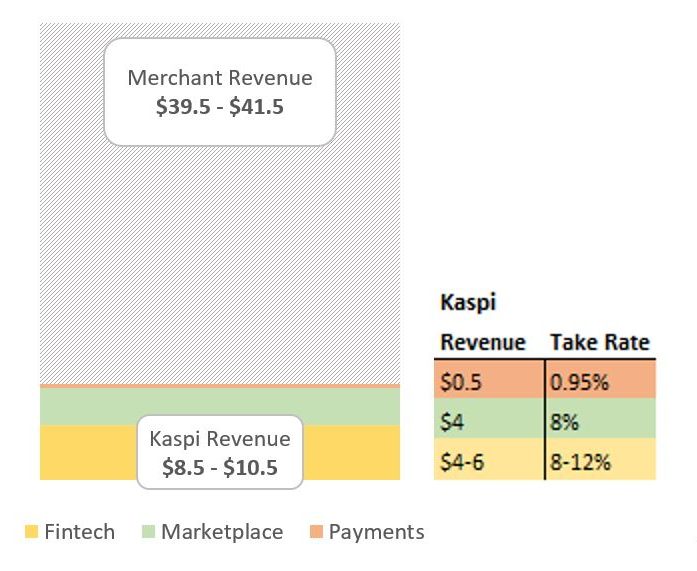

Indeed, outside of China, one would be hard pressed to find a company that has a firmer grip on the consumer spending journey than Kaspi.kz enjoys in Kazakhstan. In providing a place to purchase, a method to purchase and the means to fund that purchase, Kaspi.kz owns every commercial touchpoint of the transactions through its platform, thereby gaining access to the maximum profit pool of each consumer. Consider someone making a US$50 online purchase, funded through a three-month, 0% interest BNPL product. That single transaction has three revenue channels for Kaspi.kz, equating to between US$8.5 and US$10.5 in revenue. That is a whopping 17-21% of the overall transaction value.[5]

Figure 3: Revenue distribution for $50 e-commerce transaction funded through 3month BNPL

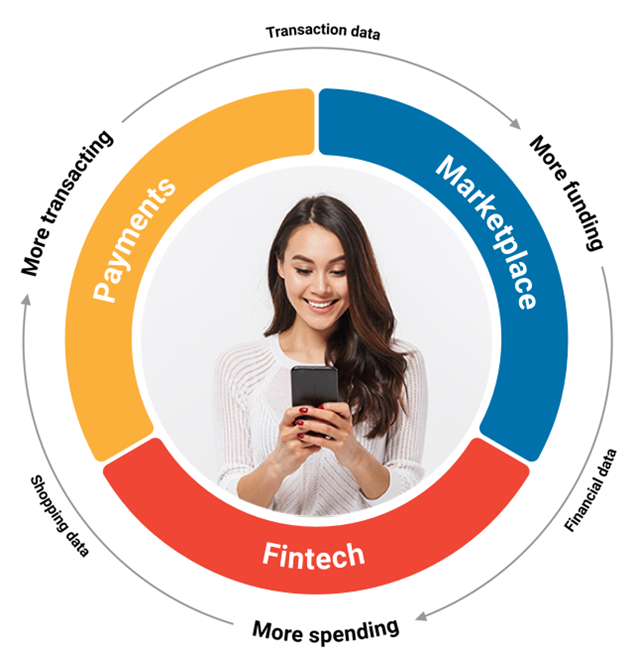

The roots of success are often multifaceted, and Kaspi.kz is no exception. No doubt there are traces of the Matthew Effect, but equally we see attempts to deploy the same payments-marketplace-consumer finance trifecta in other markets as far inferior.[6] In our view, the triumph of Kaspi.kz in Kazakhstan is not as much in the business mix as it is in how those businesses are woven together. And in this case all yarns lead back to BNPL.

Figure 4: Kaspi.kz’s three businesses benefit from a strong network effect

Contrary to the traditional BNPL model of maximising standalone yields, Kaspi.kz utilizes BNPL as the engine room to drive the average transaction value (ATV) and volume of its users high enough to maximise the revenue of the entire platform. Incremental transactions generate proprietary data points on each user that pollinate other revenue generating areas of the business, whilst simultaneously diluting cost centres such as product development, sales and marketing, and risk management. That arms Kaspi.kz with new products and data to support more informed lending decisions, and thus the cycle repeats. Such is the potency of this lending model that through 2021— a period when the three global BNPL giants collectively burnt over US$1 billion of cash— Kaspi.kz’s standalone lending business generated a return on equity of over 45%.[7]

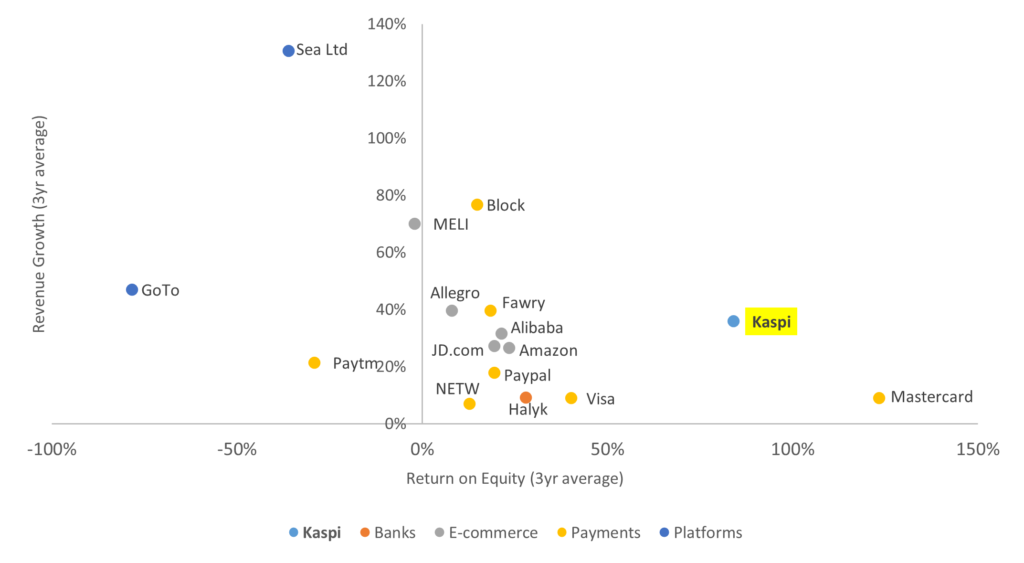

One of the most compelling upshots from this model is the impact on growth. Revenues magnified by intertwined, self-perpetuating products have a diluting effect on the cost base, sending operating leverage into overdrive. As a result, Kaspi.kz has managed to grow revenues at a 34% CAGR since 2019, despite spending on average just 4% of revenue on sales and marketing.[8] Even more astounding is that this growth was delivered at an average net margin of over 40%, for a combined growth and return profile that is best-in-class on an industry, regional and even global basis.

Figure 5: Revenue growth (three-year average) vs. return on equity (three-year average) for comparable peers

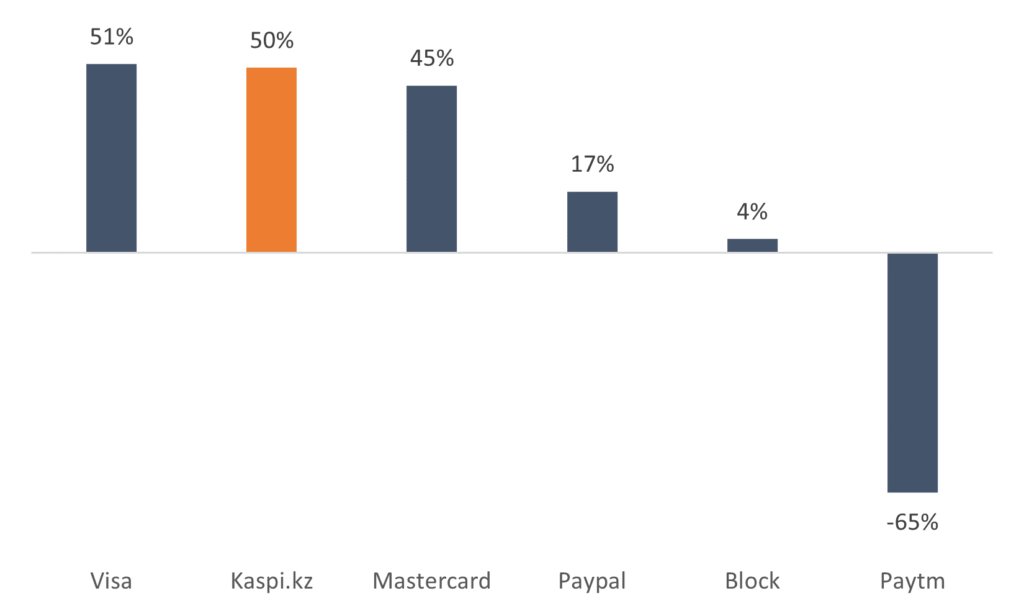

Consequently, Kaspi.kz enjoys the luxury of being able to subsidise strategic products profitably. In the marketplace business that means providing 95% of deliveries free of charge whilst still operating at over 60% net margin. Within payments, it means monetizing less than 10% of the peer-to-peer (P2P) transactions that constitute over 75% of total payments volume, thereby forgoing the lucrative interchange fee that typically represents the largest revenue line for digital banks, including Monzo and Revolut, as the cost of customer acquisition. That Kaspi.kz’s standalone payments business can still deliver net margins comparable to the largest and most successful global payments companies, despite surrendering these fees and operating in a market a fraction of the size, speaks to the harmony of its consolidated platform.

Figure 6: Net income margins of payments peers (three-year average to last reported period)

Data shown for Kaspi.kz is the standalone payments business

The term super-app is overused and, in our view, frequently misunderstood. Sifting through investment decks of the not-so-super, the moderately-super or even the one-day-we-are-sure-to-be-super apps that flood our markets can at times feel like dragging a philistine through a modern art exhibition. No matter how fervent the arguments may be that the blue square in front of you is a masterpiece – a unique perspective on modernism – to the untrained eye it all looks rather the same. When we suggest that Kaspi.kz is emerging as one of the few genuine super-apps it is not because the platform tells the same exhausted story of having multiple products under one roof. Strength here is not in numbers: It is in the intricate design of each product such that the sum of all products is greater than the parts.

Critically, the platform must have ‘plug and play’ compatibility with new products. Acting as a magnet for new services that yearn for an adrenaline shot of growth is vital for keeping the platform sharp, competition blunt, and deepening the competitive moat of any aspiring super-app.

Take for example, Santufei, a negligible rail and airline ticketing vendor that comprised just a handful of people and a few basic aggregator relationships when Kaspi.kz acquired it in August 2020 for a paltry US$5 million. Today, that business (rebranded ‘Kaspi Travel’) sells over 70,000 tickets per month through what is now the largest rail and ticketing platform in the country. And travel tickets are just the start. There is a not-so-distant future where we foresee an office worker in Almaty ordering a taxi after a long day, getting home to receive promotions for their favourite takeaway, placing an order and then tipping the delivery driver all through Kaspi.kz. In this world, it is 3rd party developers that must bow as Kaspi.kz ascends to the gilded heights of consolidator. The gatekeeper to an ecosystem so rich that 3rd parties are forced to cede a slice of the economics, despite assuming all the business risk.

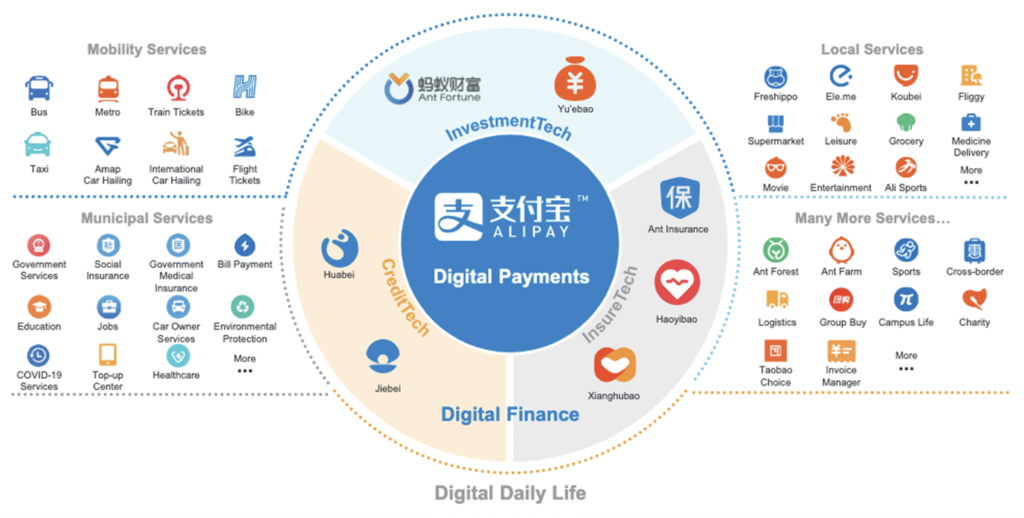

Platform compatibility is also relevant for the merchant base. Many services unbeknownst to consumers such as B2B payments, supply chain management solutions and merchant credit services offer equally attractive economic prospects, if not a means to entrench the platform deeper into the Kazakhstan economy than their consumer product counterparts. One only needs to look at the breadth of services offered through Alipay today to get a sense of how much more room there is for Kaspi.kz’s platform to grow.

Figure 7: Alipay offers insight into what the future Kaspi.kz platform may look like

Although the example of Alipay offers a glimpse as to the end state for every aspiring super-app, we must remember that by no means does it reflect the sole operating model. Platforms with origins in payments will differ to those grown out of e-commerce, financial services, or one of the countless other services that can support the initial acquisition of customers. In our view, it is the understanding of this centrality that becomes essential in helping us see beyond a familiar and otherwise undifferentiated countenance.

So while Kaspi.kz will march on, continuing to forge new products against the idiosyncrasies of Kazakhstan, the near-term focus for us will remain firmly on BNPL. For today, that is the beating heart of the company’s ecosystem. The consumer credit juggernaut that in equal measures poses the greatest risks and opportunities to sustainable growth.[9] That we maintain our diligence, stay grounded in our approach and appreciate the consumer credit business for what it really is, will give us the best chance – we hope – of seeing Kaspi.kz write its own fairy tale ending.

[1] Based on ~139 million labour force and ~17 million credit cards in circulation. Sources: World Bank; Bank of Indonesia.

[2] Grossly simplified, Kaspi.kz is probably best thought of as a combination of Revolut, Paypal and Taobao. A somewhat fitting unity of East and West.

[3] Source: Analysis of the payment market in the Republic of Kazakhstan, PWC (March 2022).

[4] Source: Analysis of the retail e-commerce market in the Republic of Kazakhstan, PWC (October 2022).

[5] Moreover, this example is conservative. BNPL products that exceed three-months draw interest from the consumer and higher take rates from merchants, while certain e-commerce categories also command higher take rates.

[6] Taken from the Gospel of Matthew and popularized as the Power Law, the Matthew Effect is based on the idea that market leaders will attain a disproportionate amount of value over time. For companies with large network effects, that typically means being first to market.

[7] The three global BNPL giants referenced here are Klarna, Affirm and Afterpay, which reported US$631 million, US$431 million and US$159 million FY21 net losses respectively.

[8] Calculated as three years to June 2022.

[9] Macroeconomic risks associated with Kazakhstan are also at large, and the exclusion here for simplicity should not be confused with insignificance.